My ETA Journey and What is ETA? - #2

I provide an update on my ETA search and some insights on the opportunities and the risks.

Damon Johnson

8/15/20253 min read

This is the second newsletter where I’m sharing my journey to acquire a small business through Entrepreneurship Through Acquisition (ETA).

In an effort to better explain ETA, I thought I would share with you some of the podcasts I have been listening to recently. The first one is called Think Big, Buy Small (https://podcasts.apple.com/us/podcast/think-big-buy-small/id1751989991) and another really great podcast is Acquiring Minds (https://podcasts.apple.com/us/podcast/acquiring-minds/id1569715379)

ETA involves buying a small to medium business with a proven track record, offering a lower-risk alternative to startups, where 80–90% fail. One of the key criteria in searching for a firm is to find one that is “enduringly profitable”. Typically, that means they have been in business through many economic cycles, but at least 8 to 10 years with consistently growing profits, recurring revenue, and loyal customers. Maybe you have heard of HVAC, plumbing or roofing companies being acquired recently? While those are great small businesses that typically match the investment criteria, given my background I will be focused on MSPs (Managed Service Providers or otherwise known as Managed IT firms). If you’ve ever worked for a small company, you have seen they typically don’t have an in-house IT department and instead they hire a firm to help set up a new PC, troubleshoot a problem, configure a server or deal with a CyberSecurity threat. These are great businesses because the modern workforce is now more remote than ever and our growing dependence on the cloud requires that companies maintain tighter security, industry specific compliance and flexibility. The demand curve for software and “always on” connectivity is inelastic, meaning these are “must have” services whether the economy is booming or receding.

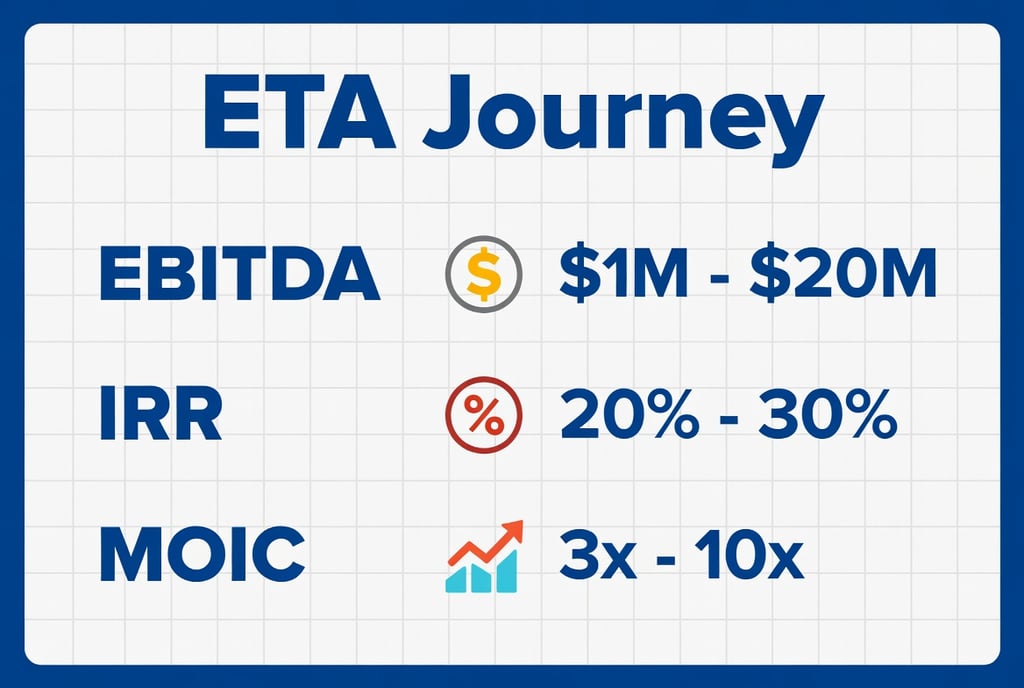

Recently, I spoke with a fellow “searcher” that purchased a Managed IT provider four years ago. At that time the company had $1M in Cash Flow (aka EBITDA - Earnings Before Interest Taxes Depreciation and Amortization) and he paid 3 times the Cash Flow or roughly $3M. During his tenure leading the company, he increased the customer base and improved efficiencies and he ultimately increased the CashFlow from $1M to $4M. Assuming the same 3X multiple he paid, he increased the value of the company from $3M to $12M. However, because the company was now more mature, almost four years later, he found that bigger investment funds were interested in his bigger company and they were willing to pay 9 times the CashFlow or $36M. He signed the deal just two weeks ago and in four years he increased their investment from $3M to $36M. In the private equity industry, they call that a 12X MOIC (Multiple on Invested Capital).

A bit of an update on my search. I have shared with some of you how this experience has been equal parts educational and humbling. I have learned so much about the SBA loan process, financial structuring, the importance of the size of the deal and the inherent risks of buying too small and the ever-so tempting “roll-up” acquisitions. I will address these in more detail in future emails, but for now, I will get back to search results. I have looked at three different Managed IT companies, one in California, one in Utah, and one in Oregon. They were all interesting businesses generating roughly $1M in revenues and $300k in Cash Flow. Buying just one creates out-sized dependence on the existing owner and the two or three employees that “might” stay. Also, while all of these companies had a reasonable number of clients and no significant concentration, the departure of one or two clients could adversely affect the Cash Flow. I was really close to entering into a LOI (Letter of Intent) with one of them, but I spoke with the owner that I featured above, and he suggested that I wait for a bigger target. He argued that a larger acquisition actually reduces risk and would allow me to work more “on the business” rather than “in the business”. While I will keep my eyes open to smaller businesses that I could quickly grow, I will focus more on bigger companies with Revenues of $1.5M or more and Cash Flows of $750k or more.

Next month, I will share my experience with three different investment funds that I spoke with, some of the nuances with the banking space and what the private equity investment returns look like. I am so grateful to all of you that have responded so positively and the support you have offered. And, I am also humbled by the generosity of time and advice from the new people I have met during this search process.

Sincerely,

Damon Johnson